Well, as you can see, the statement speaks for itself. The world is one big casino, and banks are the machines that hold all the money.

The important thing in that story is their services will always be there for you and for business holders.

However, new technologies like digital cards, online payments and other technologies have poked them in this decade many times but they survived, and this time it is deeper than they imagine. And that is Blockchain technology! Everyone is aware of them, but few of us are deep enough to know “how they work and how they can affect the Financial institutions?

That’s why we are here for you guys. This article will guide you and explain the relation between Fintech industry and blockchain industry. There will be pros and cons on both sides of the table. It’s up to you what you choose.

Nowadays young generations are always innovating something to improve our lives and make it easier than before. In 1998 a computer scientist named Nick Sazabo gave the idea of decentralized crypto currency in the form of bit Gold.

And another guy’s name Satoshi Nakamoto changed the whole perspective of many industries including financing. He established white paper on blockchain models. Not just that he also published the first digital ledger using blockchain technology and named it bitcoin. After that everything becomes history.

From 2014-17 there was a major change in transaction systems. Because of the rise of cryptocurrencies, many developers are starting to create new ones. Like Dogecoin or Eig coin are top examples of them. These two crypto technologies are more stable and less inflationary than bitcoin and ethereum. This makes the transaction more smooth, protective and makes people want to spend.

What Does Traditional Fintech Offer?

At its core, traditional Fintech offers to help companies, business owners, and consumers manage them

- Financial Services

- Savings

- Investments

- Remittance transfers

What Does Crypto Banking Actually Offer?

On the other hand, crypto banks are not exactly banks but give banking services as virtual wallets. This means they can hold money and spend it if they want to. They can also change their digital cash(coins) into physical currency, but there are some taxes by the government. They are decentralized and popular in the Market Cap. However, they have fluctuations, especially bitcoin and ethereum. Doge is less fluctuating and faster than most cryptocurrencies (in transaction process), and that’s why Elon Musk supports Doge Coins not just for a meme but for the quality.

The important question is, why now? Why the new movement?

Everyone has an expiration date, and so do banks. Sometimes they go up, sometimes go down(2007 US financial crisis).

This time, the change is real! Because the problems are deep. This is how banks and crypto works

Covid

Covid realized we cannot live upon the old Fintech services anymore. Transfer issues, money security, and travel difficulties. But when we have a problem in the Fintech world, we need to travel to banks.

But with crypto banking services it. It is all on the application with greater security and safety.

Cashless Payment

Words define themselves. Blockchain banking is like a blank check for you; you can cash it no matter how much money you have. Traditional Fintech is not possible because of security issues. They create limits, and even if you have a large amount of cash, they will call and confirm your identity. This means that Fintech applications have security issues. Crypto transactional process solves this problem because of decentralization. Using crypto, we have smart contracts that can follow the money where it goes and protect it from hacking.

Peer To Peer

As digital transactions rise from the last two decades among common folks. Many companies that are not banks but give banking services have also expanded. Like PayPal, Money Gram, Western Union, Payoneer, are top examples of them. They may not provide all the banking services, but they have given us important features. Many of these companies are trying to use crypto technology. Following that, MoneyGram just announced that people can buy or withdraw crypto from them. The same goes for Payoneer and PayPal.

Under-Bank

Under-banking, it is very famous in the USA. They have taken a lot of business from traditional banks. They mostly offer

- Savings accounts

- Debit Cards

- Checking accounts

If they try to use blockchain technology, they will cross the road miles away. Under-bank is also becoming a trillion-dollar company

so with crypto on its side, it will become one of the major industries in the world with safety, security, monitoring, and after services.

Because blockchain technology is new in some industries, they believe it is like a torrent (illegal). But that’s not the solution; we should analyze the effectiveness of blockchain on the Fintech industry, by the way the reviews are very good. Banks should not fear from this technology. They should understand the procedure, make them secure, and the use of their benefits.

If we fully deploy crypto to Fintech applications development. They will give you so much that you can only dream.

They will offer us

- Recognizing systems

- Recognizable contracts

- Timestamps with blockchain

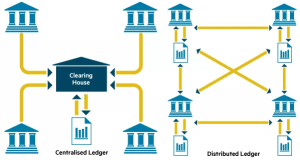

Crypto Fintech Can Change ATMs And Accounting Systems of Banks

As you know, we use ATM cards (credit or debit) for cash on daily purposes. But the backend process is very lengthy. We need almost twelve companies to hold transaction data when we use cards. Then it goes to the account ledger for different companies that store your data. Which is a much longer, time-taking and money-wasting process (additional tax).

Blockchain technology provides us with a solution, by using blockchain ledger it will take only one transaction record and only need one bank record at a time.

With blockchain technology on our side, we can protect our money with security and safety (using AAA) while transferring to another person.

There will be fewer complex data in the records; we can easily follow the money (where it went and where it came from). We can also have banking services 10 times faster than we do now.

Leave a Reply

You must be logged in to post a comment.